Dive Transient:

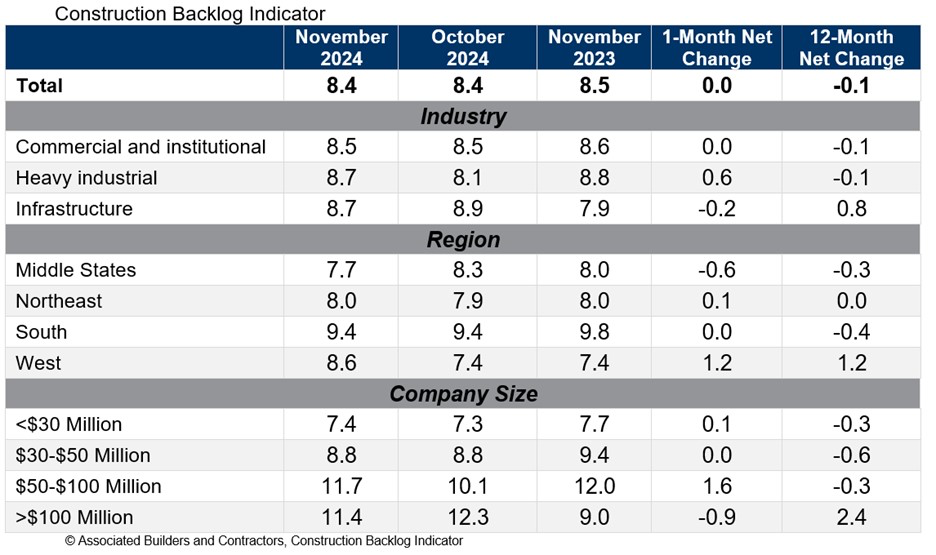

- Development backlog held regular at 8.4 months in November, reflecting resilience within the pipeline amid ongoing financial uncertainty, in line with an Related Builders and Contractors survey carried out from Nov. 20 to Dec. 3

- Contractors anticipate a rebound in privately financed initiatives, buoyed by optimism surrounding potential cuts to borrowing prices and elevated coverage readability following the presidential election, in line with the report.

- Infrastructure backlog stays a standout, posting year-over-year good points regardless of declines in different classes, in line with ABC.

Dive Perception:

The information underscores the continuing buoyancy of the development sector, regardless of financial and political shifts, stated Anirban Basu, ABC chief economist.

“Contractor confidence surged in November though backlog was unchanged for the month,” stated Basu. “This sudden enchancment in confidence displays elevated coverage certainty within the wake of November’s presidential election, and contractors are optimistic in regards to the prospect of falling borrowing prices over the following a number of quarters.”

By sector, backlog confirmed blended motion in November, in line with ABC. Infrastructure backlog fell 0.2 months in comparison with October however stays a standout with a 0.8 month improve over the previous yr.

Heavy industrial backlog jumped 0.6 months in November, however stays down 0.1 months in comparison with November 2023. Business and institutional backlog posted no change from October and is down 0.1 months over the previous 12 months.

Contractors’ expectations for elevated exercise in privately funded initiatives over the following six months hinge on additional reductions in rates of interest, stated Basu. If these cuts materialize, builders may revive delayed or shelved initiatives.